We define a digital business as a business in which value creation is based on the use of digital technologies, including:

- Internal and external processes

- How an organisation engages with customers, citizens, suppliers and partners

- How it attracts, manages and retains employees and talent

- What products, services and experiences it provides, and how

So, digital is central to organisations, from the business core to all the different parts that make up the wider business. But why are use cases important? What’s their role in the digital business?

The answer is simple. As use cases are discrete-funded projects to support a business’ goals leveraging key enabling technologies, use cases are the critical building blocks that help them to become a digital business.

IDC EMEA’s Future Enterprise Resilience Survey, October 2021 (n = 430) shows that 60% of EMEA companies say use cases are important to drive digital strategies and road maps, but that organisations need to understand how to build on them for their business and how to make them work.

While you are reading this blogpost, there are numerous executives lost the in the “use case ocean” asking themselves and their board questions such as:

- What are the key resources we need to have in place?

- Who should steer them?

- What type of technology investments should we make?

- How do we measure outcomes from this project?

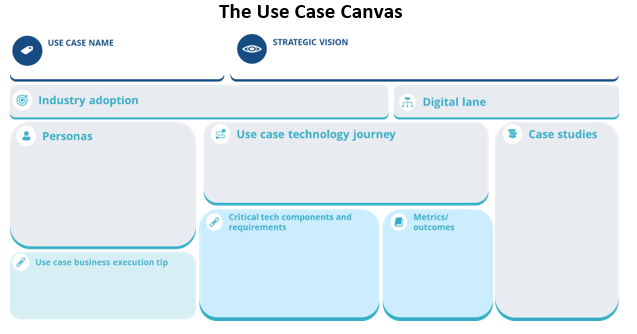

How can organisations answer these questions? By using a framework that tackles all the issues, such as IDC’s “Use Case Canvas” (see Digital Transformation Use Cases in 2022: A “Use Case Canvas” for the Top 10 EMEA Use Cases).

The use case canvas is a framework designed to easily map top level use case requirements, from IT components and resources to measurable metrics, to evaluate the successful implementation and personas required to ensure a successful implementation.

To better understand this, let’s look at a practical example in the customer experience space.

360-Degree Customer and Client Management: An Example

If you’re working on a use case to better manage customers and clients (if you’re tech vendor building your tech road map or a tech buyer seeking to improve your digital strategy) you can find yourself stuck with the questions highlighted above, so let’s take a closer look:

- The chief customer success officer, the customer experience officer and the head of customer service/support drive, influence and steer the use case. It’s important to first decide who is in charge of executing a specific use case and to talk to them about how to address their challenges.

- Use case business tips. Highlighting the guidelines and best practices from a business standpoint will ease the adoption of the use case; for instance, for the specific use case under analysis, collaboration is pivotal and this can be achieved only with the adoption of adequate tools and systems to ensure collaboration across different functions working on it.

- Use case technology journey. This is the step-by-step journey to evolve the legacy technology architecture to implement the use case. This means collecting customer data across multiple sources (physical or digital) and applying algorithms and AI to ensure real-time customer insight.

- Critical tech components and requirements. This covers the tool kit to ensure the use case is executed successfully. In this case that means CRM application, social media and online messaging, AI models and so on.

- Metrics and outcomes. Track the success of the use case with measurable metrics: net promoter scores (NPS), revenue per customer and customer churn rate. This should give you an idea of where the organisation is heading.

- Second only to metrics and personas is the case study showcasing tech buyers’ success stories on how they implemented the use case, the challenges they faced, best practices and the benefits achieved to benchmark the results. For more information, please see the Kone example in IDC’s The State of Digital Transformation Use Cases for Customer Experience in EMEA: Digital Lane Report Series — 1 of 5.

What Should You Do as a Tech Vendor?

With business leaders increasingly involved in tech matters and projects, technology projects need to focus on shifting from tech talk to business talk as they tend to see the business story behind the technology investments. How can you do that? By:

- Leveraging IDC’s use case canvas to guide customers along their digital transformation journeys and understanding exactly what your customer is asking you

- Tying your go-to-market strategy and language to personas and moving outside your IT comfort zone

- Using the canvas to enable your sales reps to drive conversations around use cases

- Doubling down on your efforts to bring peers’ case studies and examples to the table — sometimes a face-to-face customer lab is the best way forward

What’s Next?

Please read the document that this blog refers to (Digital Transformation Use Cases in 2022: A “Use-Case Canvas” for the Top 10 EMEA Use Cases) and check our Digital Business Strategies page for new research covering a range of topics such as customer experience, operations and workforce. If you’d like to know more about this report or to discuss anything with us, please contact us, especially if you’re a tech vendor prioritising your digital use case road maps and sales strategy or a tech buyer if you’d like a better understanding of the steps you need to take to implement a solid digital use case strategy.